Last week delivered a sharp reality check for tech bulls as NAS100 shed over 4%, whilst US30 and the FTSE quietly held their ground. This week, I'm watching whether the Nasdaq can stabilise above 28,890 or if we're in for a deeper correction — with geopolitical noise from Iran and China adding fuel to an already jittery market.

Last Week in Review

Last week was a tale of two markets. Whilst US30 (+0.32%) and the FTSE 100 (+0.67%) ground higher, tech got absolutely hammered — NAS100 dropped 4.05% and the S&P 500 fell 1.59%. The catalyst? A combination of AI infrastructure concerns (heatwaves threatening data centres), renewed geopolitical tension between the U.S. and Iran over the Strait of Hormuz, and China widening export restrictions on Japan. Gold pushed higher by nearly 2%, reflecting safe-haven demand, whilst oil whipsawed on supply fears before settling slightly lower. The week closed with indices showing clear divergence — old economy holding, new economy bleeding.

US30 (Dow Jones) — Weekly Outlook

US30 closed the week at 51,876, just shy of the previous close at 51,920 — essentially a neutral weekly candle with a modest +0.32% gain. The 5-day range was 51,301 to 52,655, and we've now pulled back from that high, settling in the middle of the range. My bias this week is cautiously bullish, but conditional. Support sits at 51,301 (last week's low), with the previous close at 51,920 acting as immediate pivot. Resistance is clear at 52,655 (5-day high). If US30 can reclaim and hold above 51,920 early this week, I'm looking for a push back towards 52,655 and potentially higher. The Dow's resilience last week — whilst tech crumbled — suggests rotation into industrials and value, which could continue if geopolitical tensions ease further. However, if we lose 51,301, that invalidates the bullish case and opens the door to 51,000 and below. The key this week is whether we see follow-through buying or if this is just a pause before broader risk-off takes hold. I'm watching the Iran situation closely — any escalation kills this setup.

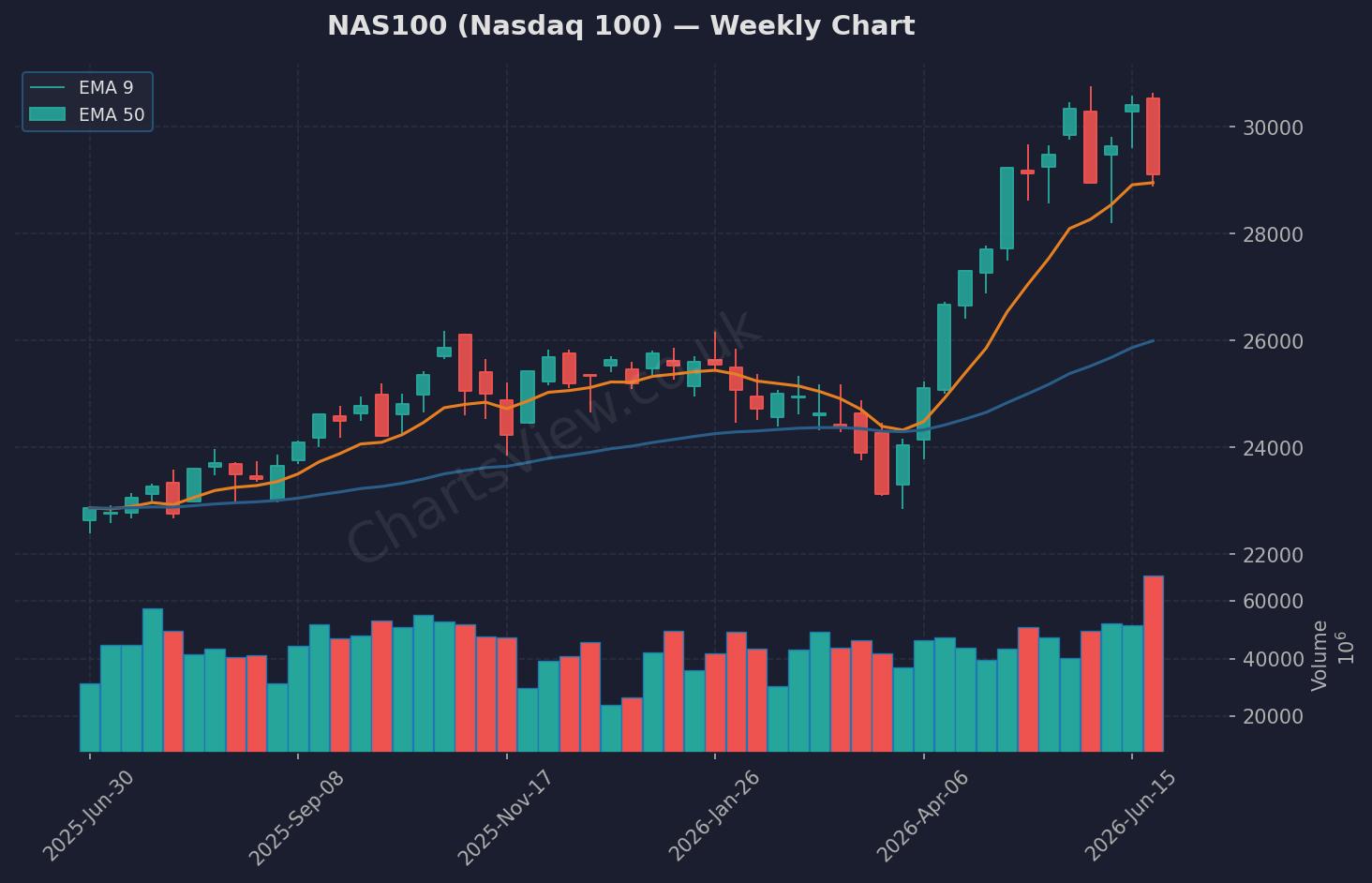

NAS100 (NASDAQ) — Weekly Outlook

NAS100 (Nasdaq 100) Weekly Chart — EMA 9 (orange) & EMA 50 (blue) | Source: ChartsView

NAS100 had a brutal week, closing at 29,118 after losing over 4% and falling from a 5-day high of 30,642 down to a low of 28,890. We're now sitting well below the previous close of 29,440, and the weekly candle is a clear bearish engulfing. My bias is neutral-to-bearish until we reclaim 29,440. Support is at 28,890 (5-day low) — if that breaks, we could see a flush towards 28,000. Resistance is stacked above: 29,440 (previous close), then 30,642 (5-day high). The AI infrastructure concerns and severe weather risks are weighing heavily on sentiment, and with Bitcoin also wobbling around $60,000 (strategists calling it a "critical battleground"), risk appetite for tech is fragile. I need to see a decisive reclaim of 29,440 with volume before I'd consider longs. Until then, rallies are fades. If 28,890 holds and we get a bounce, I'm watching 29,440 as the line in the sand — above it, we're back in play; below it, stay defensive.

Quick Takes

S&P 500: Down 1.59% to 7,354 — caught between tech weakness and Dow strength; watching 7,294 support and 7,530 resistance for direction.

Gold: Strong week at +1.96%, now at 4,068 — safe-haven bid remains intact; support at 3,963, resistance at 4,104.

GBP/USD: Slipped 0.31% to 1.3206 — holding above 1.3143 support, but needs to reclaim 1.3250 to regain bullish momentum.

WTI Oil: Down 2.88% to 69.85 despite Iran tensions easing — watching 68.56 support; break below could see 67.00.

Key Events This Week

- Monday, 09:00 GMT — EU Economic Sentiment (Jun): Forecast 94.3 vs 93.5 prior. A beat could support European equities and put pressure on the dollar.

- Monday, 08:30 GMT — UK Mortgage Approvals (May): Forecast 63K vs 65.94K prior. Weakness here would add to concerns about UK consumer health and weigh on the FTSE.

- Monday, 17:30 GMT — ECB President Lagarde Speech: Any hawkish tilt could strengthen the euro and pressure EUR/USD, which is already down 0.32% on the week.

- Monday, 14:30 GMT — Dallas Fed Manufacturing Index (Jun): Previous 0.4 — a decent gauge of U.S. industrial activity; watch for any deterioration.

The biggest risk event is Lagarde's speech — any shift in ECB tone could ripple across global risk assets, especially if she signals concern over inflation or growth.

The Week Ahead — My Game Plan

I'm approaching this week with a selective bias — bullish on US30 if we hold 51,301 and reclaim 51,920, but defensive on NAS100 until it proves it can reclaim 29,440. The divergence between indices is the story here, and I'm not forcing trades in tech until the structure improves. Geopolitical headlines around Iran and China remain a wildcard, so I'm keeping stops tight and position sizes conservative. If you're trading this week, know your invalidation levels before you enter — this isn't a market that's rewarding hope. Trade what you see, not what you think should happen.

Written by Remo, founder of ChartsView. This outlook reflects personal analysis and does not constitute financial advice. Always do your own research and manage your risk.