Tech bulls took control last week as NAS100 surged nearly 3% while traditional indices struggled, with the FTSE shedding over 2% and US30 closing marginally lower. This week brings a historic earnings gauntlet — five of the Magnificent Seven report — alongside stalled Iran peace talks keeping oil volatile and geopolitical risk elevated.

Last Week in Review

Last week delivered a clear rotation into tech, with NAS100 climbing 2.68% to close at 27,303.67 whilst traditional indices lagged badly. The FTSE 100 dropped 2.17% to 10,379.08, weighed down by energy sector weakness as Brent crude fell 0.86% despite ongoing Middle East tensions. US30 closed fractionally lower at 49,230.71 (-0.43%), whilst the S&P 500 managed a modest 0.79% gain to 7,165.08. The week's story was simple: investors piled into tech ahead of this week's earnings deluge whilst dumping energy and defensives on stalled US-Iran negotiations.

US30 (Dow Jones) — Weekly Outlook

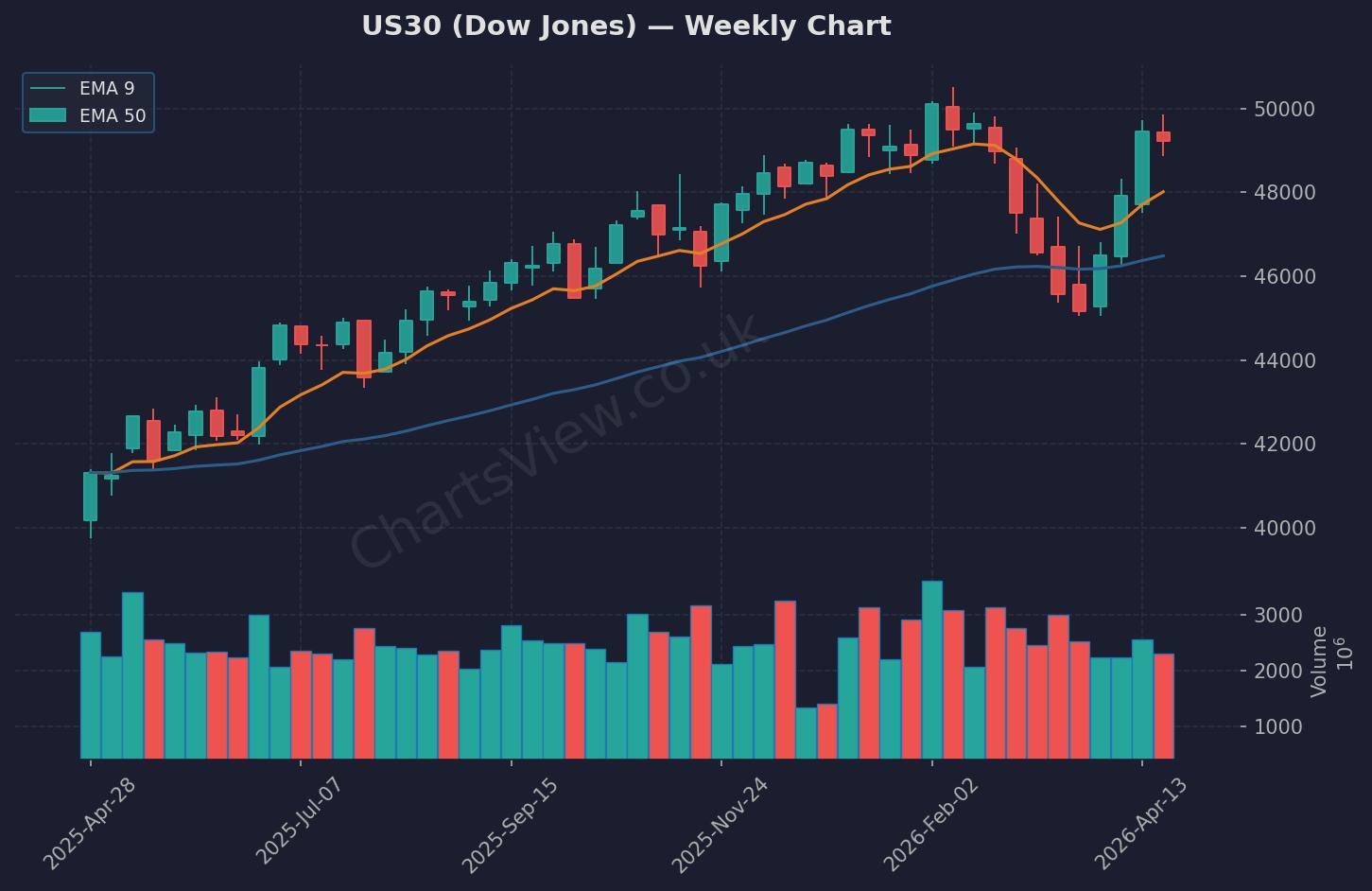

US30 (Dow Jones) Weekly Chart — EMA 9 (orange) & EMA 50 (blue) | Source: ChartsView

US30 closed the week at 49,230.71, printing a small bearish candle with a 0.43% decline after failing to hold above the 49,310 previous close. Price tested the 5-day low at 48,861.31 mid-week before recovering, but the rejection at the 49,848.69 high tells me buyers aren't convinced yet. The index is now sandwiched between clear levels: support sits at 48,861 (last week's low), with secondary support at 49,000 psychological. Resistance is immediate at 49,310 (previous close) and then 49,848 (5-day high).

My bias this week is cautiously bearish below 49,310. The Dow's underperformance relative to tech suggests money is rotating away from industrials and financials, and with geopolitical risk still elevated, I'm not chasing longs here. If we break below 48,861, I'm looking for continuation towards 48,500. That said, a reclaim of 49,310 with conviction would flip me neutral, and a break above 49,848 invalidates the bearish view entirely. The setup I'm watching: a retest of 49,000-49,100 zone for shorts targeting 48,600, stops above 49,400.

NAS100 (NASDAQ) — Weekly Outlook

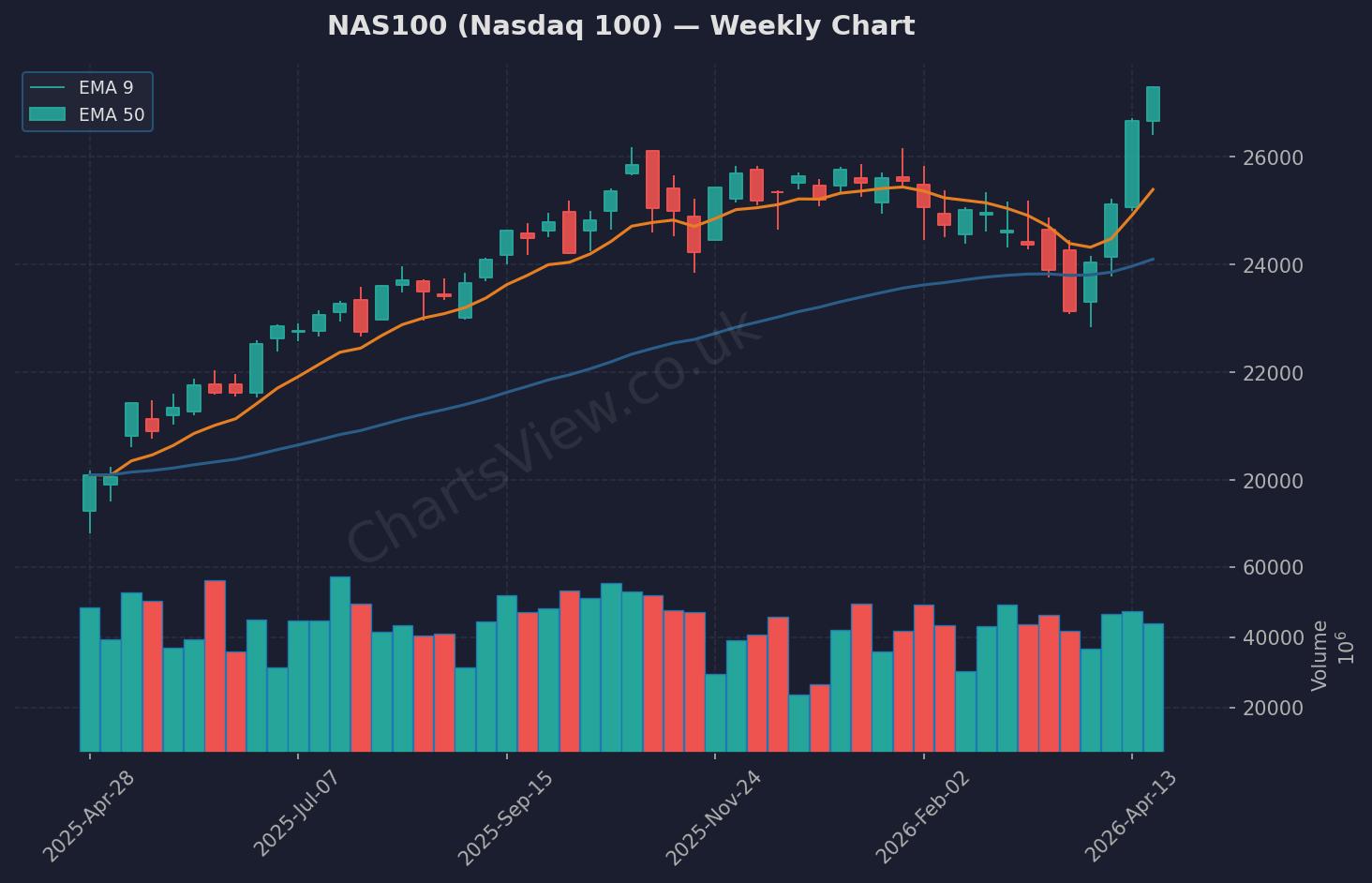

NAS100 (Nasdaq 100) Weekly Chart — EMA 9 (orange) & EMA 50 (blue) | Source: ChartsView

NAS100 was last week's star performer, rallying 2.68% to close at 27,303.67 — just shy of the 5-day high at 27,314.21. This is a bullish weekly candle with strong momentum heading into the most important earnings week of the year. Five of the Magnificent Seven report this week (Meta, Apple, Amazon among them), and the market is clearly positioned for upside.

Support is clean: 26,782 (previous close) and then 26,405 (5-day low). Resistance is minimal — we're essentially at all-time highs with 27,314 the only barrier before blue sky. My bias is bullish above 26,782. If we hold Friday's close and break 27,314, I'm looking for continuation towards 27,500-27,600. The risk is an earnings disappointment that triggers profit-taking, so I'm keeping stops tight. A close back below 26,782 would concern me and suggest the rally is exhausted. For now, the path of least resistance is up.

Quick Takes

S&P 500: Closed at 7,165.08 (+0.79%), holding above 7,108 support — bullish structure intact but watch for tech earnings to drive the next leg.

FTSE 100: Weak close at 10,379.08 (-2.17%), now testing support at 10,361 (5-day low) — needs to reclaim 10,457 to stabilise or we're looking at 10,200.

Gold: Flat at 4,734.00 (+0.03%), consolidating between 4,657 support and 4,754 resistance — geopolitical premium keeping it elevated but no clear direction yet.

WTI Oil: Rallied to 95.95 (+3.22%) despite stalled peace talks — watching 98.39 (5-day high) for breakout or 94.40 support for pullback entries.

Key Events This Week

- Monday 06:00 GMT: Germany GfK Consumer Confidence (May) — Forecast -29.5 vs -28.0 prior. European sentiment data as recession fears linger.

- Monday 10:00 GMT: UK CBI Distributive Trades (Apr) — Forecast -48 vs -52 prior. Retail sector health check amid cost-of-living pressures.

- Monday 14:30 GMT: US Dallas Fed Manufacturing Index (Apr) — Previous -0.2. Regional manufacturing pulse.

- Wednesday (time TBC): Fed Chair Powell's final press conference alongside mega-cap tech earnings (Alphabet, Amazon, Microsoft, Meta) — this is the single biggest risk event of the week. Volatility will spike.

- Ongoing: US-Iran peace talks remain stalled — any headline developments will move oil and risk sentiment sharply.

The Week Ahead — My Game Plan

This week is all about tech earnings and whether the AI rally can justify these valuations. I'm bullish NAS100 above 26,782 and looking for continuation if the Magnificent Seven deliver, but I'm keeping position sizes smaller than usual given the binary risk. US30 looks heavy below 49,310, and I'll be watching for a retest of 49,000 for potential shorts. The geopolitical backdrop remains messy with stalled Iran talks, so oil could whipsaw violently on any headlines. My focus is on letting the market show its hand early in the week before committing size — Wednesday's earnings will set the tone for May. As always, if the setup isn't there, there's no trade. Protect your capital first, profits second.

Written by Remo, founder of ChartsView. This outlook reflects personal analysis and does not constitute financial advice. Always do your own research and manage your risk.